Co-Investments Co. Ltd Investment plans options short summary:

This blog post is an initial idea I have drafted for my client to cater different needs. Plan 1: guarantee return - 6 - 8% return for a fix period of 5 years pay out every 6 month - Min of £30,000 Benefits:

Plan 2: share ownership - Client will submit mortgage application and own a percentage of a property under their name. - No money upfront - Share of monthly profit depend on your mortgage contribution and deposit. - Commitment of minimum of 5 years. Benefits:

please send e-mail to [email protected] if you need more updated information concerning our plan & offers, or visit www.yauherbert.weebly.com This is the information I received regarding the application of mortgage for Scotland property from Bank of China.

Under our lending criteria, the minimum salary requirement is £18,000 per annum. And the minimum loan has to be over £50,000. And if you are buying a new built property, please start the process around 4 month before the completion date because our mortgage offer is only valid for 6 months (the mortgage offer has to be signed and returned within 4 months). We currently have 2 mortgage products Lifetime Tracker and 3 years Fixed Rate. Lifetime Tracker rate is floating with the changes of Bank of England Base rate. 3 years Fixed rate has a initial rate which is fixed for the first 3 years and then changes back to floating rate after 3 years. Please find some of the key features of these 2 products: Lifetime Tracker 1 year tie-in period Unlimited overpayment facility 1% early repayment charge applies to the original loan amount, payable on full redemption only within the tied-in period 3 years Fixed Rate 3 years tie-in period Overpayment facility of maximum 20% of the original loan amount per annum within the tie-in period 1% early repayment charge applies to original loan amount, payable on full redemption. Apart from the capital repayment, we can also provide interest only on BTL application with loan amount between £50K to £1m. Please find the below rate details: Lifetime Tracker -Buy-to-Let: Option 1 Loan amount: between £50k & £500k. Capital repayment Loan-to-Value (LTV): 60%; Interest Only LTV 55% Arrangement Fee: £1,895.00 Interest rate: 3.34% Option 2 Loan amount: between £50k & £500k. Loan-to-Value (LTV): between 60% to 75%; Interest Only LTV 55% to 70% Arrangement Fee: £1,895.00 Interest rate:3.64% Option 3 Loan amount: between £500k and £1m. Loan-to-Value (LTV): maximum of 70%; Interest Only LTV 60% Arrangement Fee: £3,195.00 Interest rate:3.74% 3 Years Fixed Rate – Buy-to-Let: Option 1 Loan amount: between £50k & £500k. Capital repayment Loan-to-Value (LTV): 60%; Interest Only LTV 55% Arrangement Fee: £1,895.00 + Booking Fee: £399.00 Interest rate: 3.53% - Final rate after 3 years: 4.34% ( 4.09%+based rate) Option 2 Loan amount: between £50k & £500k. Loan-to-Value (LTV): between 60% to 75%; Interest Only LTV 55% to 70% Arrangement Fee: £1,895.00 + Booking Fee: £399.00 Interest rate: 3.83% - Final rate after 3 years: 4.64% (4.39%+based rate) Option 3 Loan amount: between £500k and £1m. Loan-to-Value (LTV): maximum of 70%; Interest Only LTV 60%Arrangement Fee: £3,195.00 + Booking Fee: £399.00 Interest rate: 3.93% - Final rate after 3 years: 4.74% (4.49%+based rate) Please find the attached Agreement In Principle(AIP) which is initial stage to apply for a mortgage with us.(Note: we have not put the attachment in the blog, please contact us if you want a copy) We will do an affordability check based on the information provided. If you could pass the stress test, then I will submit your AIP to our underwriter for pre-approval (this normally takes 2-3 working days), once your AIP is agreed, I will then send you the list of documents required for full application. The process time for Mortgage offer at the moment is around 3-4 weeks after receiving all the required documents by post. Here are the costs:

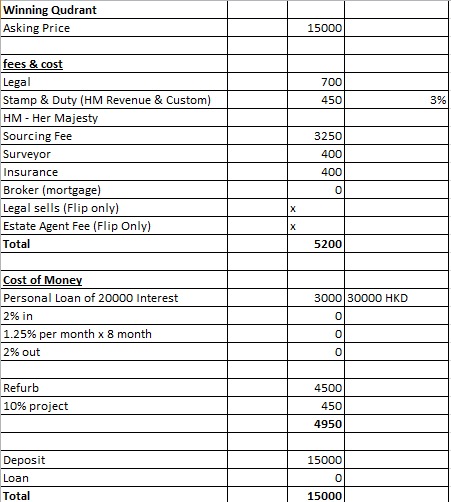

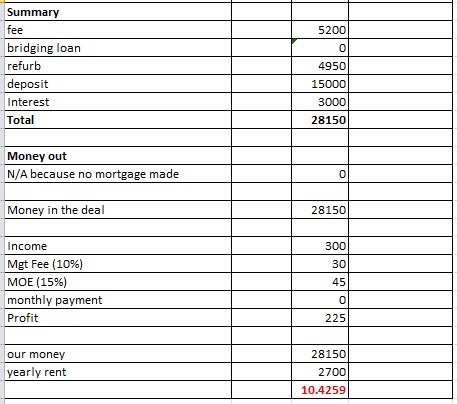

Solicitor Fee £650+ VAT (average) Survey Fee (£364 at the time of refinancing) Stamp duty only applicable over £40,000 purchase and always 3%. Insurance annually £160 Landlord registration. 3 yearly £54 per council area £11 per property My wish is to borrow money from personal loan or look for partners to invest together to speed up my investment journey to give it a head start. As the property in Scotland is relatively cheap, as an overseas investor, you won't be able to borrow money out of just 1 property, you need about 4 properties to make a lump-sum mortgage altogether. My heart was racing in all directions and I m so much eager to make a start at all costs. That's why I wrote to my sourcing agent Sarah (Source to Let) today to ask for all the costs we need to bear as an investor. So that I know how much money to raise for my first project and overall for 4 projects to make a mortgage. In previous blog posts " Getting Started with a Personal Loan" (link), I calculated that if I borrow £20,000 (or HKD200,000) with a £8000 start up fund or deposit. Assuming the rent is £300 per month, after deducting monthly outgoing expenses (MOE), that would leave me £225 per month. Our HSBC monthly repayment is £338 for 5 years. I would read the figures like this: Money in the deal Start up fund £8000 Personal Loan £20,000 Monthly Income Rent £300 MOE £75 Profit £225 Loan Repayment £338 ___________________ Loss £113 ( 5 years) I would read this figure positively! 3 Key Benefits by paying £113 for 5 years: 1. You will officially own the property in 5 years 2. You will get passive income £225 for the rest of your life 3. You will be able to remortage these properties (once you have 4 of them) and finance other project Winning Qudrant, Wishaw, ML2 7TS

Basic Figures Rental £300 Renovation £4500 Purchase £15,000 Home Report R £19,000 Investment Calculations: We need to make sure fees are accurate and to be on the safe side, we should create a 10 -15% buffer in case anything goes wrong.  Cost Summary:  Summary: includes all cost to acquire the property

Money out: Suppose we would refinance the property by adding value or renovating the place. Once we get refinance, we get money out. During the acquiring of the first few properties, we couldn't remortgage. Getting a mortgage If we were to get mortgage in the first place, the current available channel in Hong Kong is through Bank of China or Bank of East Asia. They would only lend a minimum of £50,000 (70% of the property value), meaning that your property shall reach a minimum of £72,000. Monthly Payment I have left it as a blank but it is worth our discussion. Our money is totaled 28150 yearly rent is £225x 12 = 2700 Divide 28150 / 2700 = 10.42 years, meaning Assuming no rent increase, we would have own that property in 10.42 years and start collecting passive income for the rest of your life. Let's not forget that if you have acquired several of these properties, you will be able to make mortgage out of these properties and buy more properties for passive income. For any question, you can e-mail [email protected] Herbert. I am currently looking for ways to come up with an initial investment to start my first property investment

There is an offer when I go through the 3 day training of Tigrent. They mentioned about a bridging loan before you can officially apply for a mortgage. Bridging Loan Normally, this is what is on offer 2% in (drawing down the loan) 1.25% per month (normally you would need 6 - 8 months ) 2 % out ( returning the loan) For example say a HKD 200,000 loan you will pay 2% in = 4000 1.25 % per month, say 8 months = 200,000 x 1.25% x 8 =20,000 2% out = 4000 Total interest pay = 28,000 I would usually take the total interest paid divided by the loan to evaluate the interest to loan ratio = 28,000 / 200,000 = 14% ( for 8 months repayment period) I m also applying different personal loans to get myself started. I applied both HSBC and Bank of East Asia: HSBC HSBC offered me a 200,000 Personal Loan combining interest. I will repay 230,004 Loan Amount = 200,000 Monthly Payment = 3833.4 Repayment Period = 5 years - 60 Installments Total Repayment Amount = 3833.4 x 60 Installments = 230,004 Interest to loan ratio Interest / Loan = 30,004 / 200,000 = 15% ( for 5 years repayment period) Bank of East Asia Loan Amount = 200,000 Monthly Repayment = 3973 Repayment Period = 5 years - 60 Installments Total Repayment Amount = 3973 x 60 Installments = 238,380 Interest to loan ratio Interest / Loan = 38380 / 200,000 = 19% ( for 5 years repayment period) Bank of China Loan Amount = 400,000 Repayment Period = 5 years - 60 installments Total Repayment Amount = 458,360 Interest to loan ratio Interest / Loan = 58,360/400,000 =14.6% ( for 5 year repayment period) Reader might be thinking how we could compare a bridging loan of a 8 month period to a personal loan of 5 years I would view it like this, say we compare Bridging Loan to HSBC Personal Loan

I will put this Personal Loan scenario in my next post. Stay Tuned! |

AuthorA Hong Kong entrepreneur who started multiple businesses in his career, finally lands himself in property business, documenting how he started and hope those who aspire a different life can benefit. Archives

September 2017

Categories |

RSS Feed

RSS Feed